Loan Origination System

RMs describe the work they do as “both science and art”.

PROJECT OVERVIEW

Transforming the Bank’s credit journey for Large Corporates by modernising how Relationship Managers (RMs) raise credit applications — reducing manual effort, streamlining approvals, and significantly boosting productivity.

WHY THIS PROJECT MATTERS

Group Wholesale Banking serves SMEs, Large Corporates, and the public sector — contributing 46% of the bank’s total revenue in H1 2024. Notably, Large Corporate loans accounted for 56% of the bank’s $304B loan book, making this an area of critical strategic value.

THE CHALLENGE

The Bank’s credit application process was burdened by fragmented legacy systems and heavy manual processes:

Disjointed Systems: RMs had to comb through multiple standalone systems to locate information. Information and/or supporting documentation had to be sourced from scattered channels, including outdated email threads.

Manual Data Entry: RMs have to key in same information multiple times across different sections of the application. This created inefficiencies — especially when updates were needed based on Approver feedback, requiring RMs to trace and adjust multiple fields manually.

Lack of Structure: Applications lacked a consistent structure and flow, leading to inconsistencies and delays.

Approver Identification: RMs had to manually search policies and email records to determine the right approvers for routing the application.

Regional Complexity: Different countries have different data requirements beyond the bank’s standard input, adding to the operational burden.

Time loss due to inefficiency:

59% of an RM’s time was spent on processing and reporting, time that could otherwise be spent on growing client relationships and the bank’s portfolio. This highlighted a critical need to modernise and streamline internal systems.

OUTCOME

Launched in Q1 2025 across 13 countries, the new Credit Application system delivered measurable impact:

Reduced 90% of fields in the application form by consolidating and structuring inputs based on business logic.

Fewer systems to access: Minimised the number of platforms RMs need to toggle between.

Eliminated low-value work: Automated repetitive steps to free up RM bandwidth.

Improved speed to market: Enabling quicker credit decisions by reducing manual hand-offs in the credit process and building stronger customer trust.

MY ROLE

I served as the Product Designer embedded across design and delivery phases:

Worked closely with Product Owners (many of whom were ex-RMs) in improving the Bank’s credit journey by providing UX recommendations and design solutions with legacy systems in consideration.

Drive design sessions and crafted key user flows and desktop screen designs.

Produced interactive Figma prototypes to drive stakeholder alignment and buy-in.

Supported the Squad through detailed flow walk-throughs and design QA across UAT to Production.

Collaborated with CX Designers to ensure consistency across the platform, maintaining DLS standards and documentation.

EXPERTISE

Stakeholder Management

Product Design

Prototype

Design System

PROJECT DETAILS

Client: Local Bank

Role: Product Designer

Team:

Product Owners (Previously RMs)

Service & Product Designers

Software Engineers

Scrum Master

Business Analysts

Subject Matter Experts

Tools: Figma, Jira, Confluence

Timeframe: Nov 2023 - Present

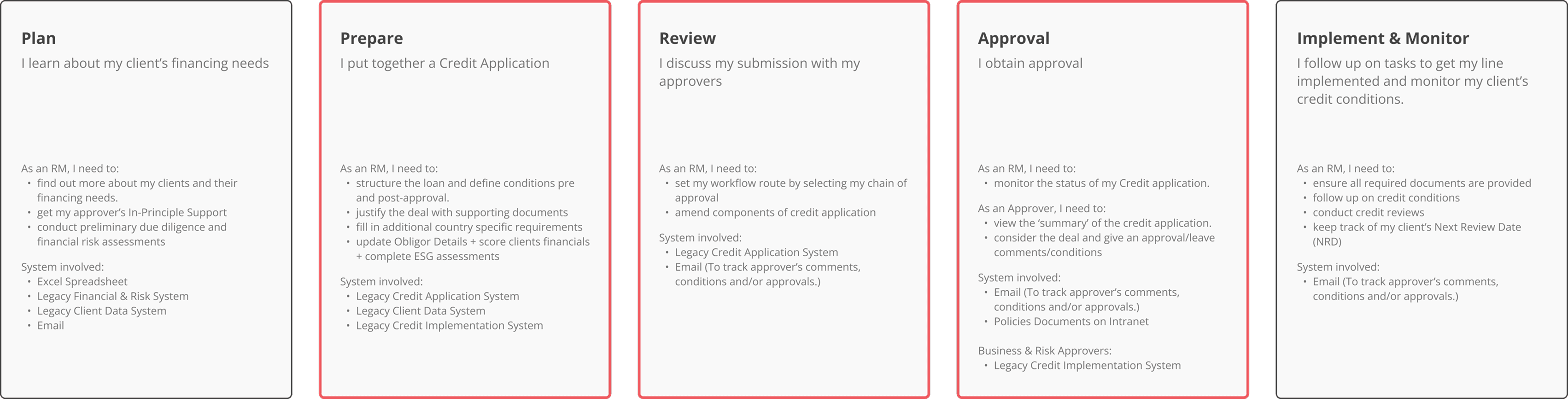

THE USER JOURNEY

With LEAP, Relationship Managers (RMs) can now manage the entire credit journey (from assessment to approval) within a single streamlined system.

Integrated Data Pull: Key client information is automatically retrieved from legacy systems, reducing the need for manual data collection.

Guided Approval Routing: The system intelligently suggests the appropriate approval levels based on the credit structure, removing the guesswork and manual policy checks.

End-to-End Digital Workflow: From preparing the Credit Application to routing for approvals and implementation, the entire process is now digital — replacing fragmented tools and email-based approvals.

Automated Data Flow: Once approved, relevant credit data flows back into downstream systems to initiate implementation, reducing rework and ensuring data accuracy.

By modernising how RMs raise credit applications, LEAP significantly reduces manual effort, accelerates turnaround times, and ensures consistency across the loan origination process.

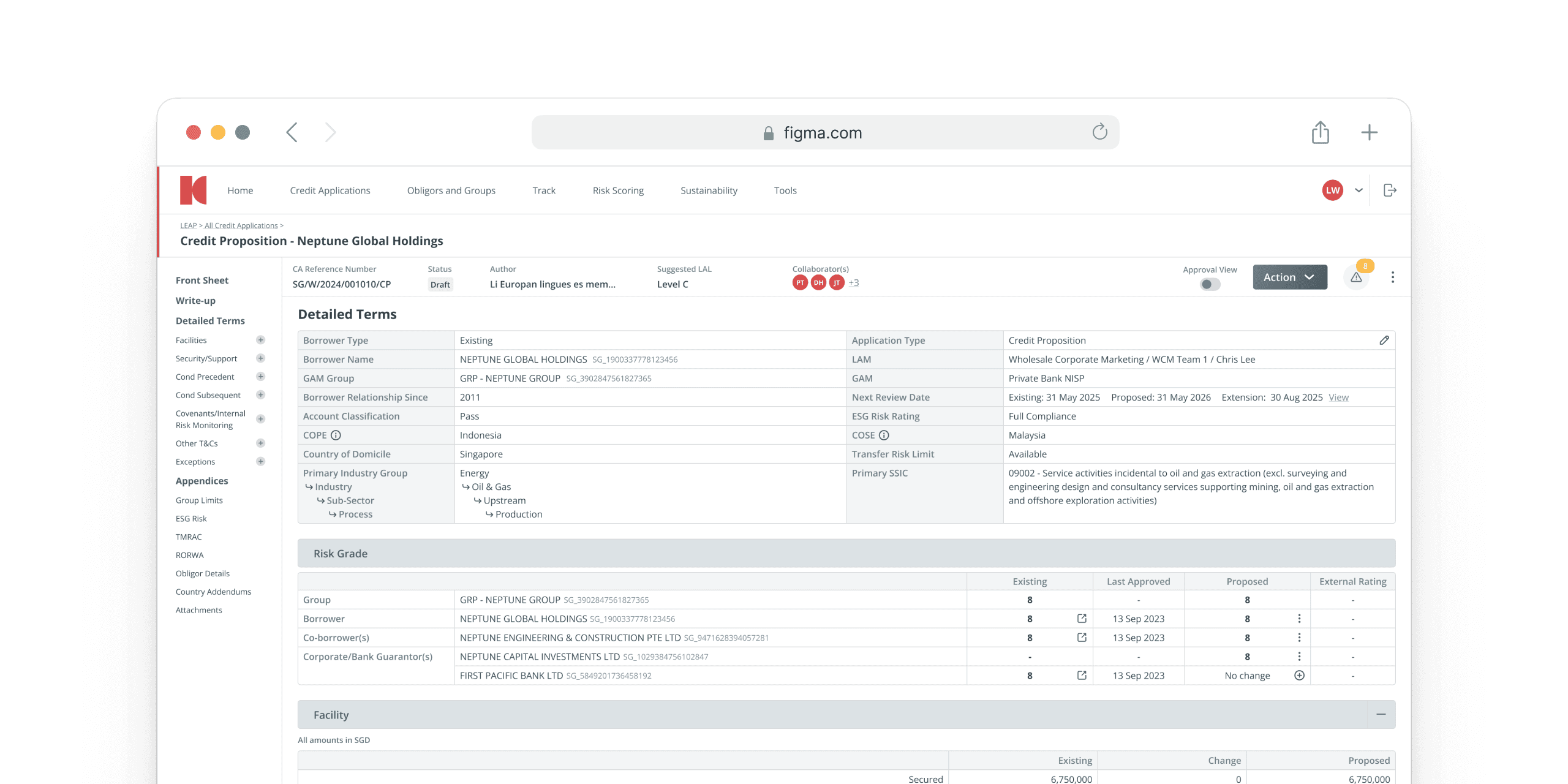

What I worked on within the Credit Application

Facility

The loan product or credit line that the bank is offering to the customer.

Outlines the structure of the borrowing arrangement — what type of loan the customer is getting and under what terms.

Security/Support

The collateral or guarantee provided to mitigate the bank’s risk.

Assures the bank that if the borrower defaults, there’s a fallback collateral or guarantee to recover the funds.

Country Addendum

Handles country-specific regulatory requirements for Singapore, Malaysia, Hong Kong, and China.

Includes additional fields needed to support local compliance during credit processing.

Features within Credit Application

Re-sequence of Terms

Creation from Abort/Decline + Copying Terms from an Existing Borrower

Credit Extension

Reduce the amount of time require for RMs to recreate the Credit Application from scratch; streamlining what was previously a time-consuming, manual process.

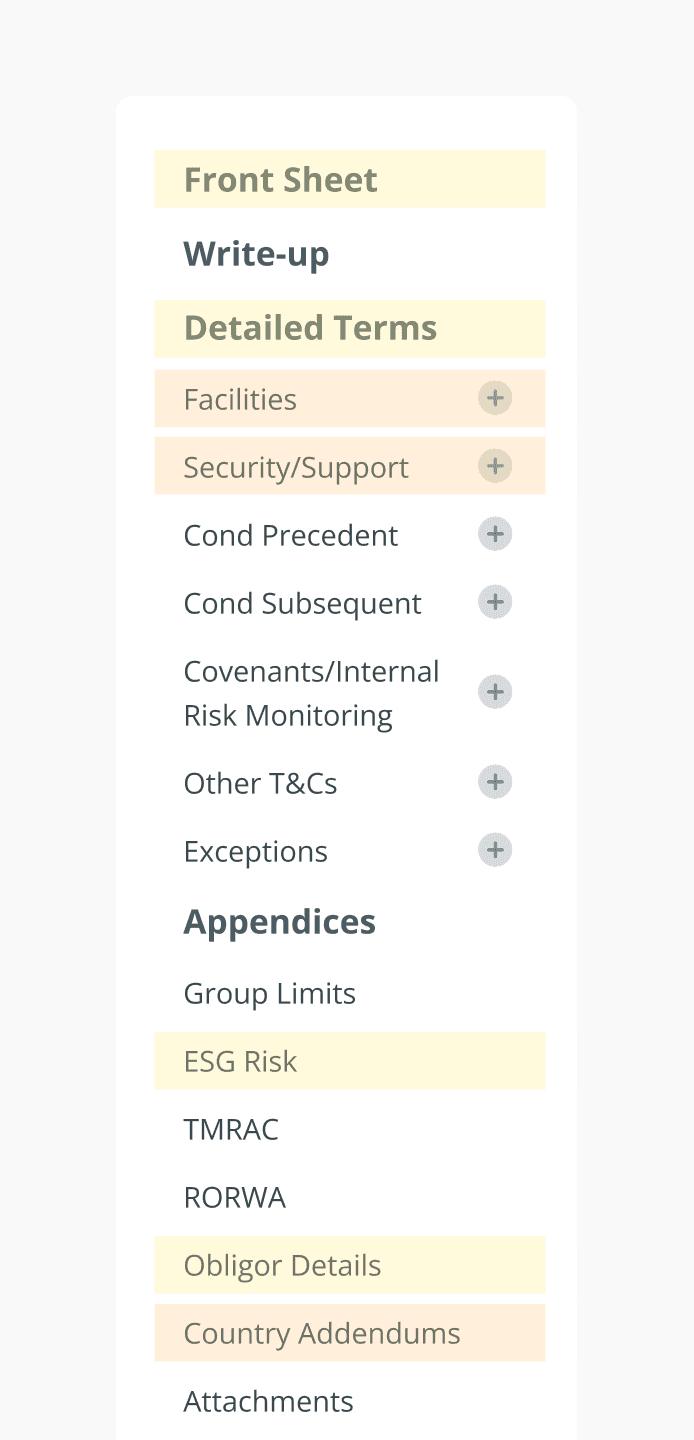

Facility

Problem 1: Unclear Facility Hierarchy; High Error Risk

Findings:

In the previous design, users struggled to identify the parent–child–grandchild levels quickly. For example, clicking ‘Add’ from Facility 1.1 created a sub-facility (1.1.1) instead of the next same-level facility (1.2), often leading to multiple back-and-forth.

Why It Mattered:

Without clear visual cues, users had to re-examine existing rows to determine their current level before adding a new entry. This increased cognitive load and slowed down task completion, especially for complex multi-tiered structure.

Proposed solution:

Use icon to visually differentiate the hierarchy and added on-hover annotations to guide user actions when adding new row.

Facility

— The “what” in the Credit Application

Why It Mattered

Facility module forms the structure of the Credit Application. Inefficiency will affect users from completing the Credit Application on time.

Defines what is being proposed — Loan products, loan amount, tenor, associated limits, purpose of the loan, repayment terms and any conditions.

Usability testing and stakeholder feedback revealed key barriers that hinders task efficiency and contributed to user confusion.

Problem 2: Rigid Workflow Mismatched Real-World Behaviour

Findings:

After speaking to some RMs, we found that some RMs preferred setting up the ‘Facility Limit & Structure’ for all items first before entering the respective detailed information. Others preferred to complete one facility at a time. The module previously did not support this flexibility, forcing a fixed, linear workflow that introduced unnecessary friction.

Why It Mattered:

Facility can be a complicated structure and user need to fill in numerous fields for each facility (in Facility Details). The previous process forces user to adapt to different mental models, slowing down task completion and increasing user frustration.

Proposed solution:

A combination of tabs and dual CTAs — ‘Save’ and ‘Save & Proceed to Facility Details’. The solution accommodate both user behaviours without being disruptive.

Tabs: To break up massive data input via progressive disclosure.

‘Save’: Caters to the first type of mental model — allowing user to quickly set up facilities structure.

‘Save & Proceed to Facility Details’: Caters to the second type of mental model — allowing user to complete facility details sequentially.

As part of this enhancement, I also reviewed and aligned the behaviour of all ‘Save’ buttons across the Credit Application to ensure interaction consistency.

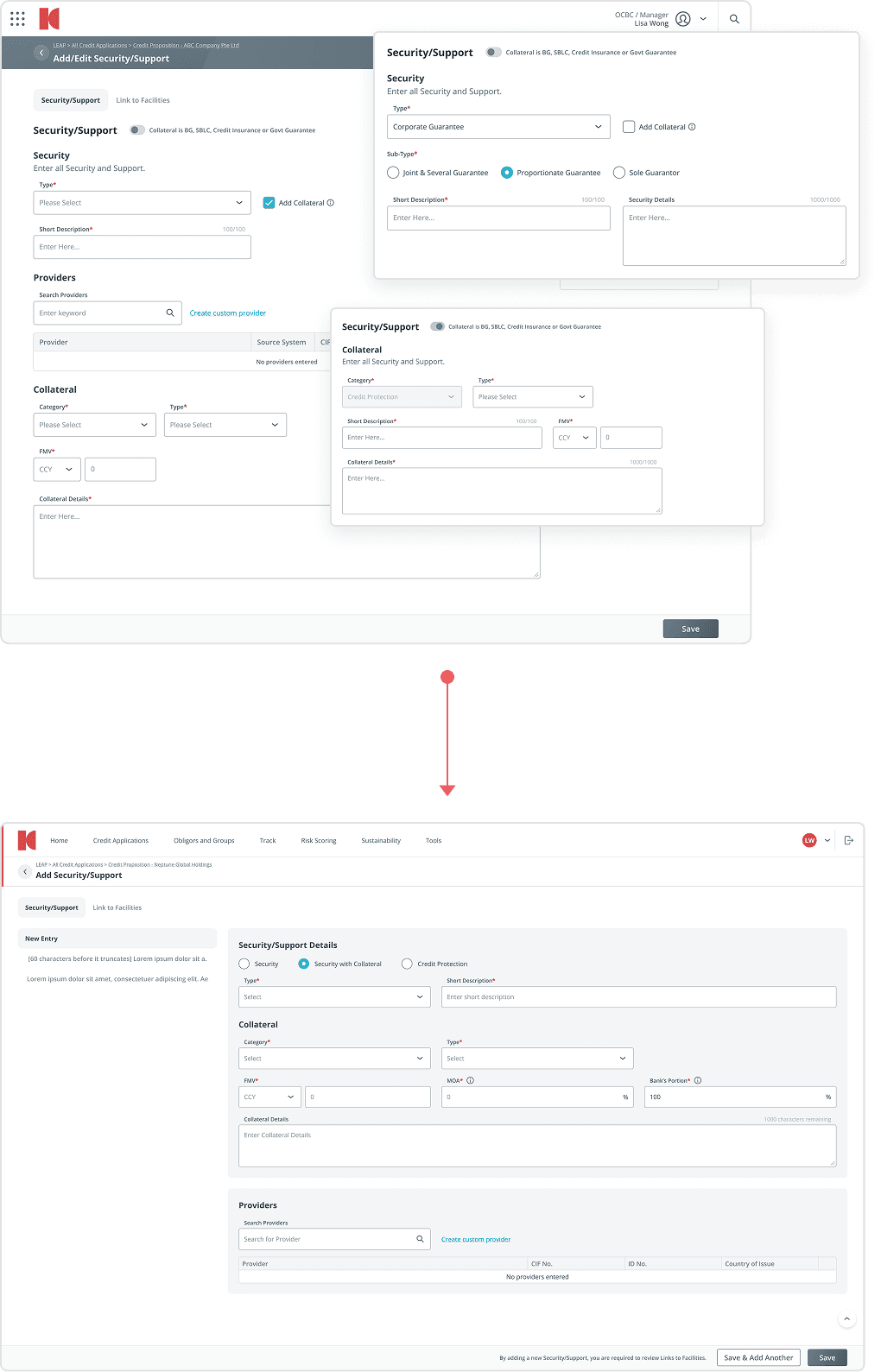

Security/Support

Security/Support is where the bank ensures risk is mitigated. However, the experience was unintuitive that users often second-guessed their actions or failed to complete critical steps. I led a complete redesign based on usability feedback and new business requirements, aiming to restore clarity, confidence, and control to this high-stakes task. By mapping out the ideal flow and prototyping key interactions, I was able to showcase the proposed experience and secure stakeholder buy-in.

Problem 1: UI Inconsistency & Unclear Form Structure

Findings:

The original design deviated from the platform drastically, confusing users.

Additionally, the lack of structure and incorrect use of UI components causes unnecessary friction. Besides generic information, most security types requires additional set of data specific to them.

Why It Mattered:

UI inconsistencies disrupt user expectations and added unnecessary cognitive load.

Incorrect use of component and poor layout design causes users to fill in unnecessary and irrelevant data frequently.

Thoughtless information architecture and poor visual hierarchy does not lend confidence to form filling and submission.

Proposed solution:

Progressively and conditionally avail related information based on previous input to reduce task aversion and keep user focused on task at hand.

This allow user to form fill and submit with confidence due to the ease of input and rework if changes are necessary.

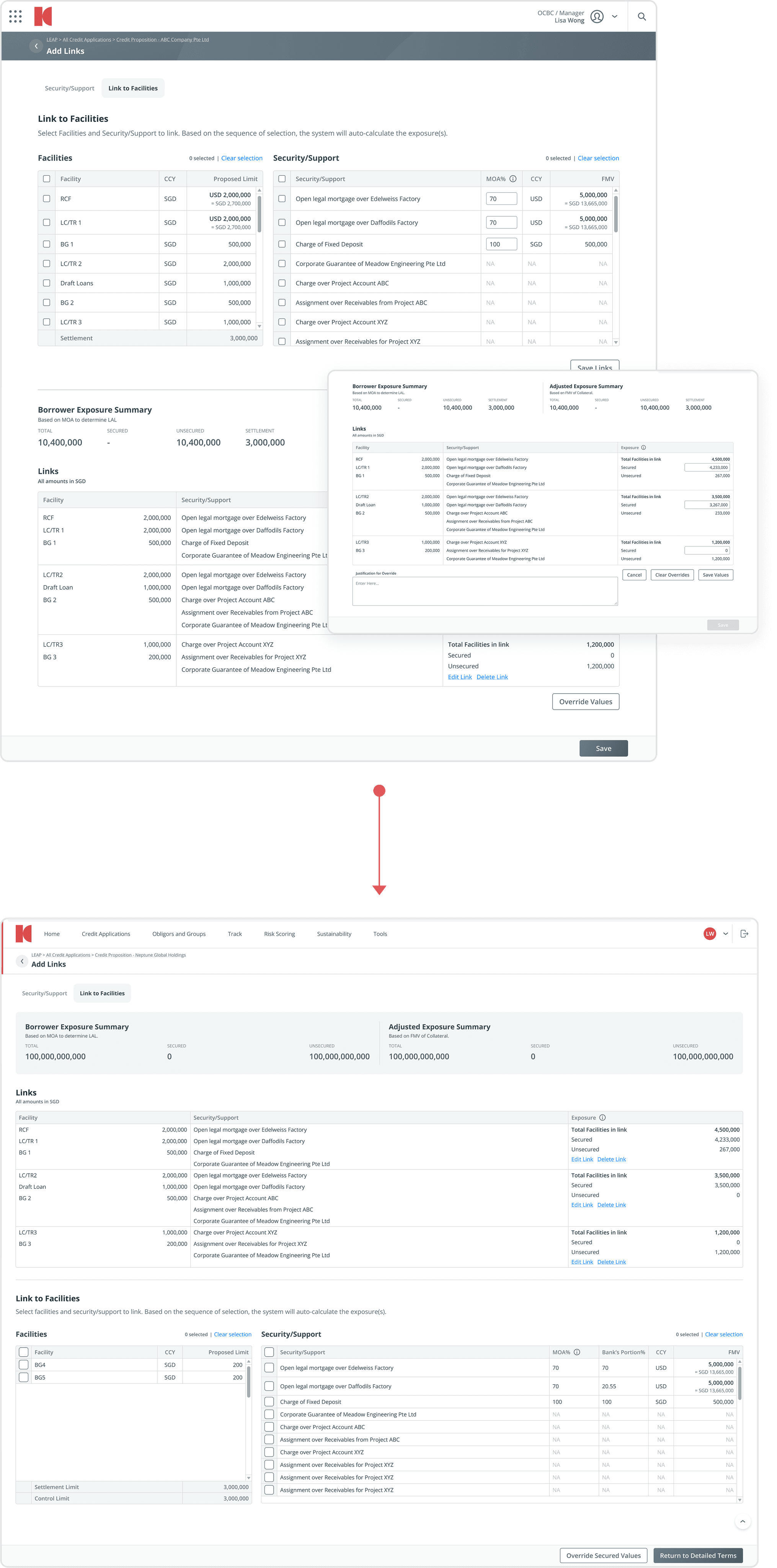

Problem 2: Disjointed Experience in ‘Link to Facilities’

Objective:

Linking of security/support to facilities is critical in credit application as it determines borrower’s risk and exposure. Users have feedback that the current experience feels disjointed.

Secured

Exposure Value

=

Fair Market Value (FMV)

x

Margin of Advance (MOA)

x

Bank’s Portion

The exposure value will determine the size, risk of the loan, and the various levels of approvals required for each Credit Application.

Findings:

The interaction was convoluted. Users were unsure how to proceed, slowing down application submission.

Multiple Save buttons (‘Save’, ‘Save Links’, ‘Save Values’) without instruction fails to provide clarity on their purposes.

We observed that users are frequently clicking on the wrong “save”.

Users were not aware of the need to click on “Save Links” for MOA edits to take effect.

Why It Mattered:

Users lacked confidence in whether data was saved or system calculations had updated.

This led to aimless clicking, incorrect exposure data, and user frustration.

Proposed solution:

Move MOA edits to Security creation, keeping linking page focus on linking of facilities.

Redesigned footer buttons to page level action that is contextually aware of users current task on hand.

Buttons will dynamically change according to user’s trigger.

E.g. if users are linking facilities, button will display “Save Links” and “Cancel”, if users are overriding secured values, buttons will display ‘Save Override Values’, ‘Clear Override Values’, and ‘Cancel’.

Country Addendum

Unifying regional credit compliance into a scalable and structured digital experience.

I led the end-to-end design of the Country Addendum module to support the Bank’s strategic direction to unify credit processes across countries. While Singapore and Malaysia were already on the legacy platform, workflows in Hong Kong and China remained manual, unstructured, and prone to risk. Each of these countries has specific compliance procedures and unique data requirements that extend beyond the Bank’s standard data fields, which were previously scattered, handled manually or managed out-of-system.

By mapping the regulatory fields and identifying overlaps with the existing Credit Application, I designed a system-level solution that is scalable, preserving platform consistency while reducing task-switching and cognitive load for RMs. This modular yet integrated approach enables RMs to focus on one layer of information at a time, complete submissions more efficiently, and enabled Approvers to easily locate and validate region specific information.

Risk of Fragmented Regional Workflows

Operational inefficiency: RMs relied on PDFs, Excel Documents, and emails to complete compliance checks, wasting time finding the latest documents.

Inconsistent data: Some regional fields duplicated existing fields under different names, leading to confusion and conflicting values.

Manual inputs: In China, more than 40 regulatory fields needs to be re-entered due to the lack of downstream integration, increasing unnecessary workload and the likelihood of data inconsistency.

High-risk and rework: In Malaysia, inaccurate CCRIS reporting will result in penalty fees and require RMs to abort and recreate the entire Credit Applications as post-submission edits are not allowed in order to maintain a clean database.

No visibility on country-level group limits: RMs and Approvers need to view the group limits at entity-level, an essential information for them to evaluate credit risk in a granular, country-specific format.

Design and business decision to reduce risks and support compliance with scalability in mind

Separate region-specific compliance data into a dedicated Country Addendum module

Keep the common build clean and focused on bank-wide requirements.

Clearer Credit Application IA structure helping RMs to focus on regional compliance only when necessary.

Reflect existing data from the common build into the Country Addendum where appropriate

Maintains continuity and avoids re-entry, preserving contextual meaning while reducing friction.

Enables RMs to complete compliance steps without shifting mental context.

Support region-specific UX needs

For example, Malaysia RMs requires a bespoke view to efficiently assess data for CCRIS reporting. This view allows fast filtering and side-by-side comparison, reducing error risk and enabling more confident review.

Validate design with POs, regional POs and other stakeholders to ensure business feasibility and regulatory alignment.

This modular yet integrated design future proofs the bank by establishing a foundational framework that new updates and regions can easily adapt and enhance. Also, RMs are now able to complete submissions with fewer errors, higher confidence, and significantly reduced back-and-forth.

Features within Credit Application

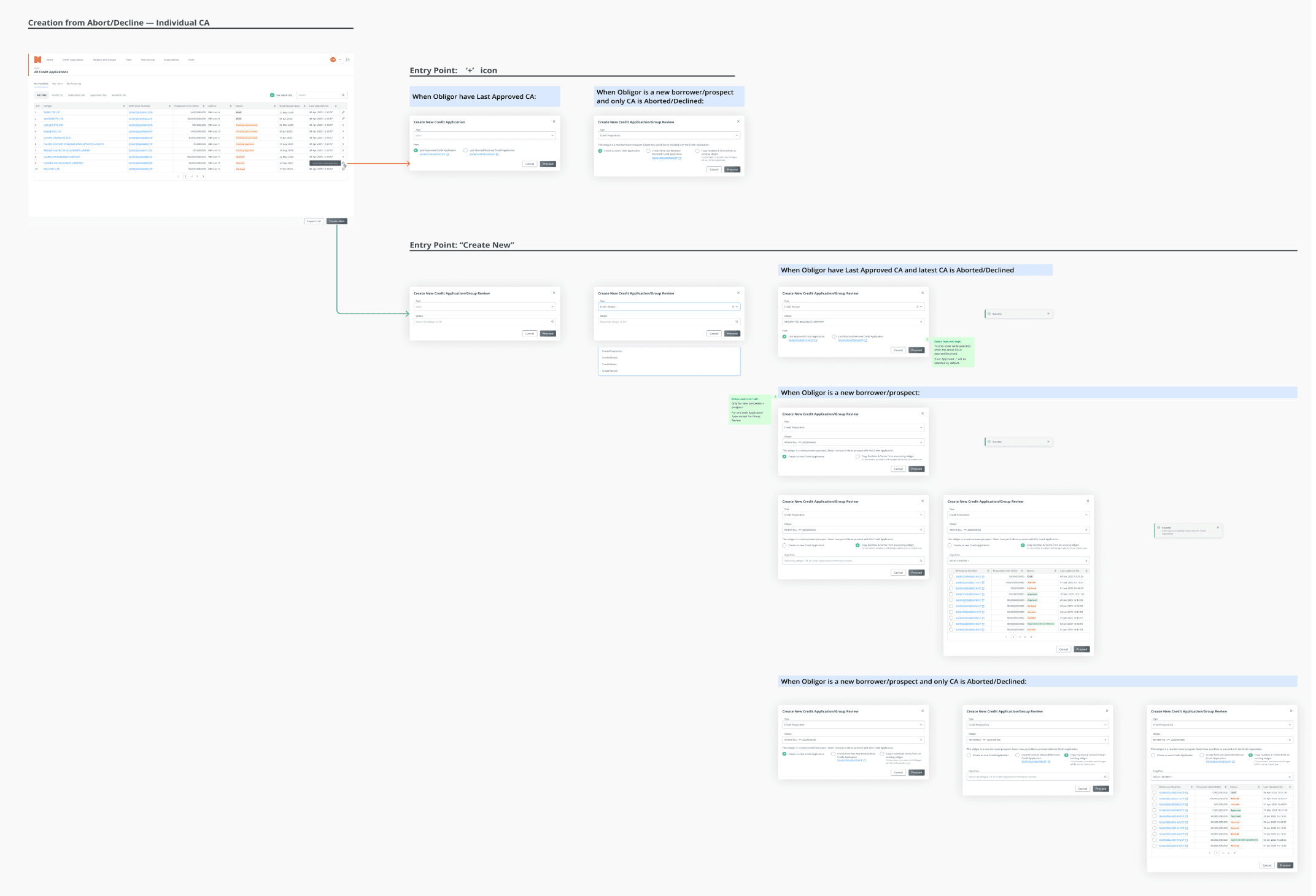

Streamlining Credit Application Creation

This feature allow:

Re-creation from the latest Aborted/Declined application for the same borrower

Creation from another existing borrower for new borrower cases

Key Design Considerations:

System logic

Aborted/Declined: The option only appears when the borrower’s most recent application is in an Aborted or Declined status.

Copy set-up: Applicable only for new borrower with no existing application.

Multiple entry points

I mapped the user journey and inserted the option in relevant touch points during application creation so it’s contextual.

Outcome:

Reduces manual re-entry effort and saves time across markets

Increases RM productivity, particularly in regulatory-heavy regions like Malaysia.

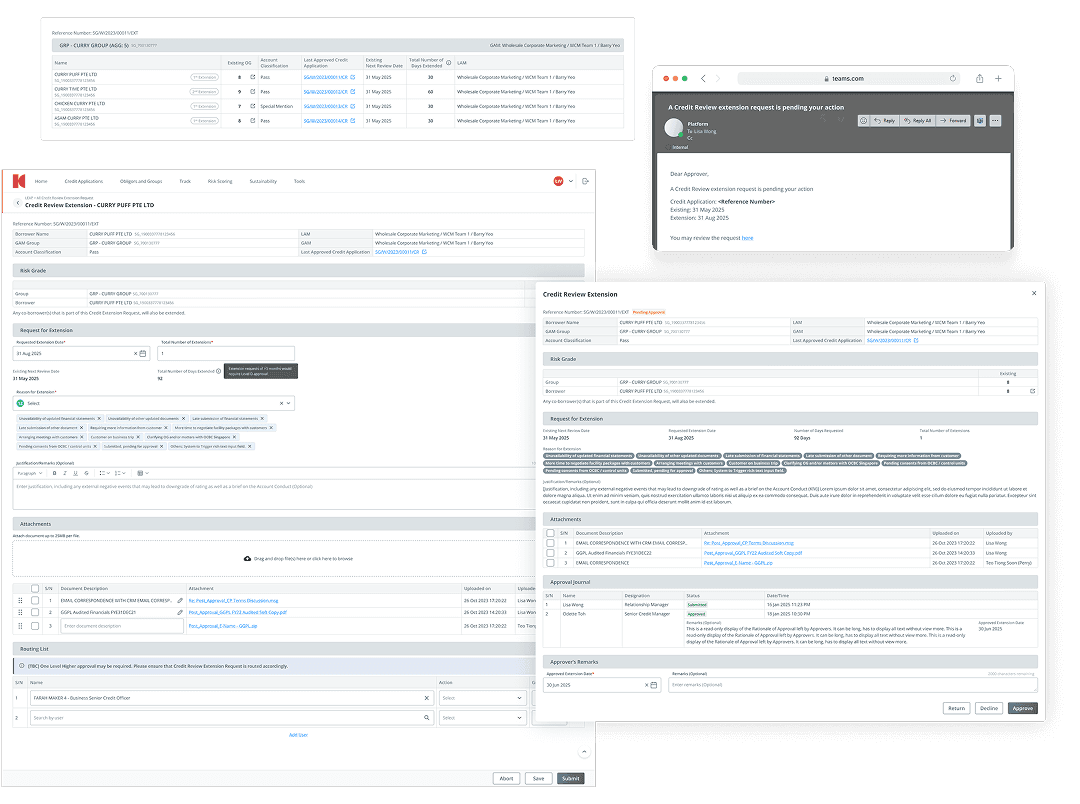

Credit Extension

RMs often need more time to submit Credit Applications due to borrower delays, missing documents, or ongoing negotiations. Previously, extension requests were made via email which creates visibility issues, inconsistent routing, and no audit trail.

CR Extension feature outside the credit application flow, allowing RMs to formally request additional time through the system with visibility and structure. It enables:

RMs to submit extension requests, track the number of past extensions and route based on approval policy.

Approvers to approve, return, or decline requests, with optional remarks.

Both users to view a complete Approval Journal for transparency and audit trail.

Change Management Considerations:

Some RMs preferred email due to its simplicity.

To reduce resistance, we kept the experience lightweight and focused on clarity, providing only what’s necessary without adding friction

Other Responsibilities

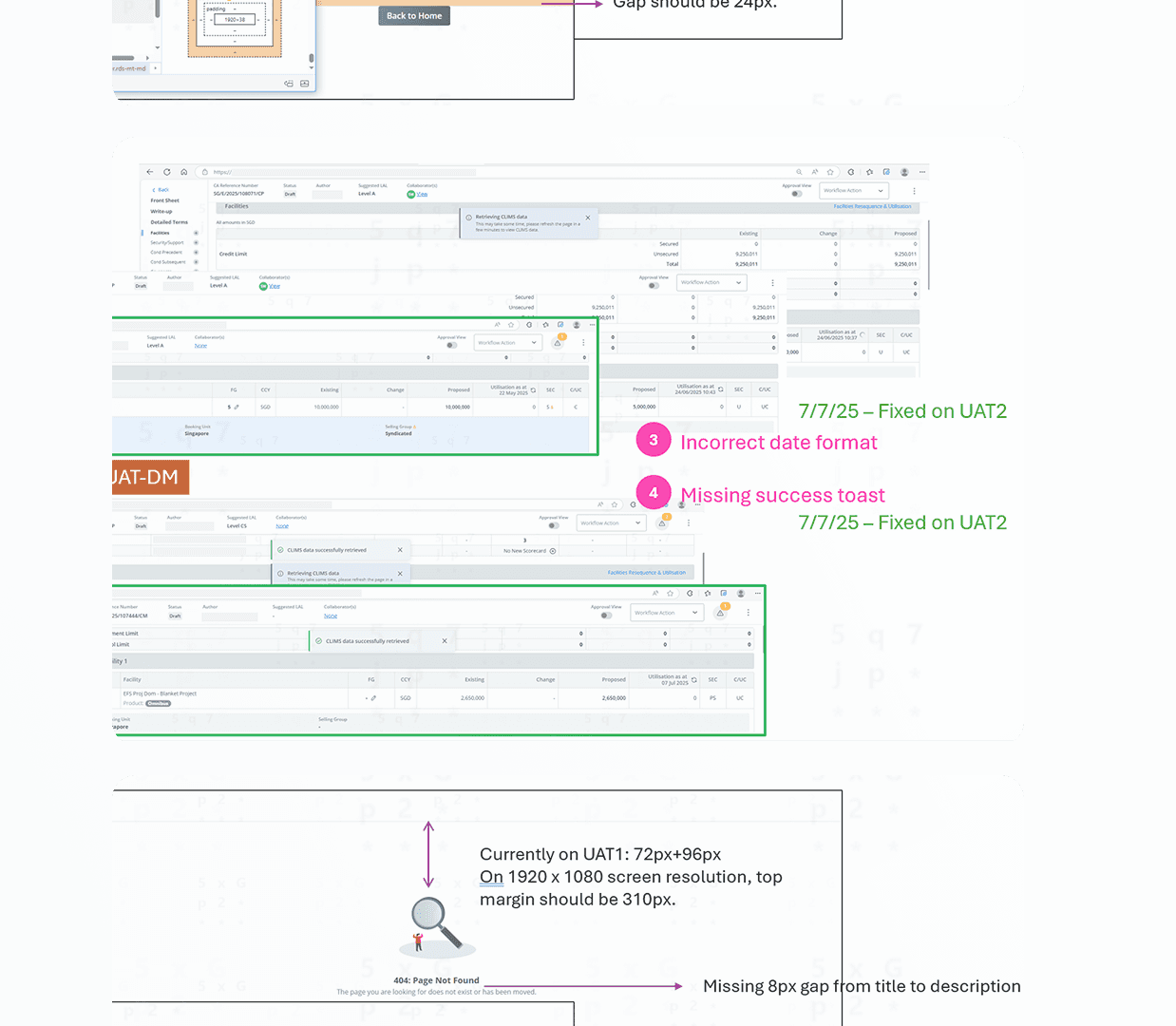

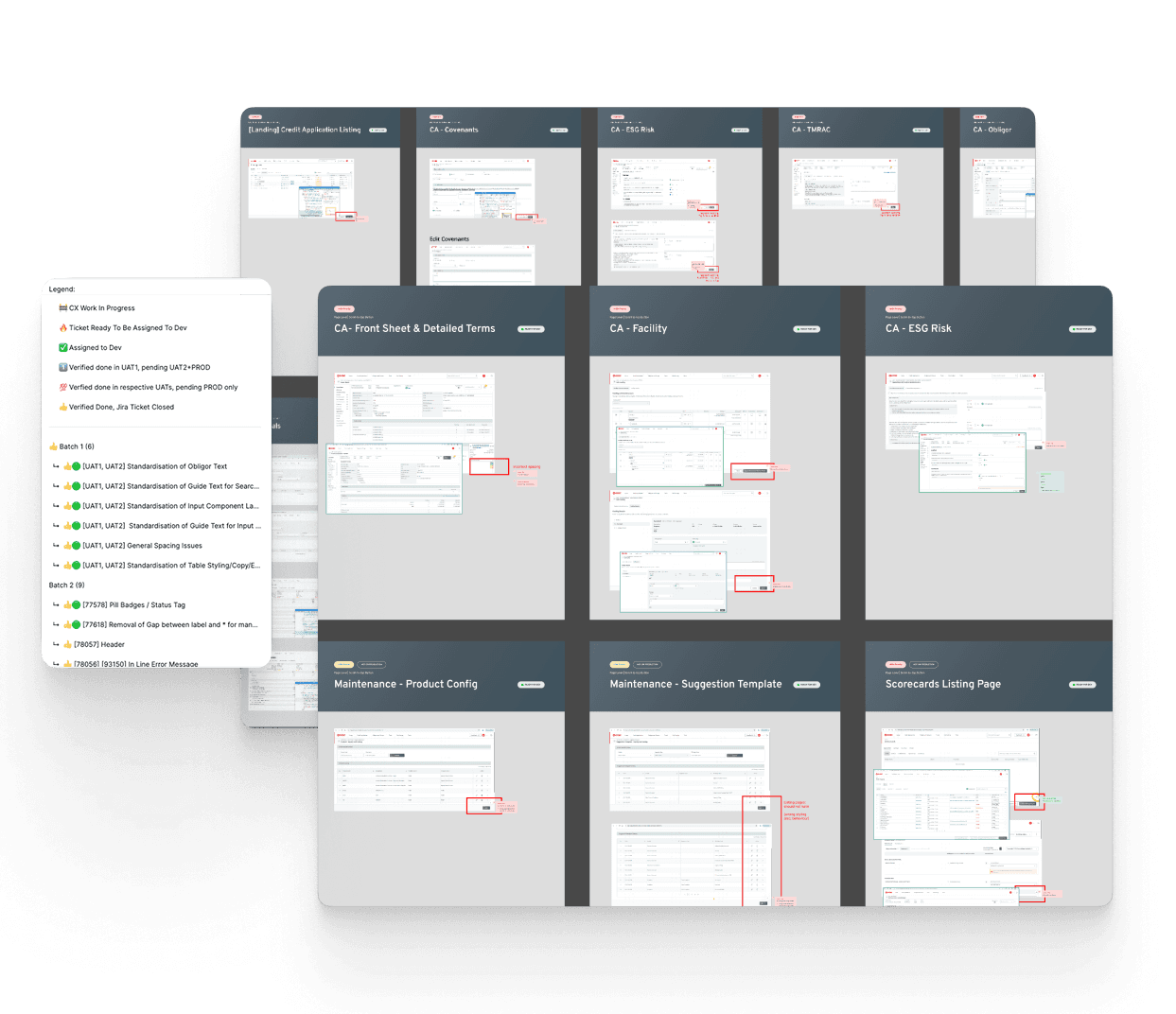

UAT Checks

Provided design QA support in sync with sprint cadences. Validate UI alignment, logic and interaction flows in test environment before UAT deployment. Surfaced design gaps and supported developer queries throughout implementation.

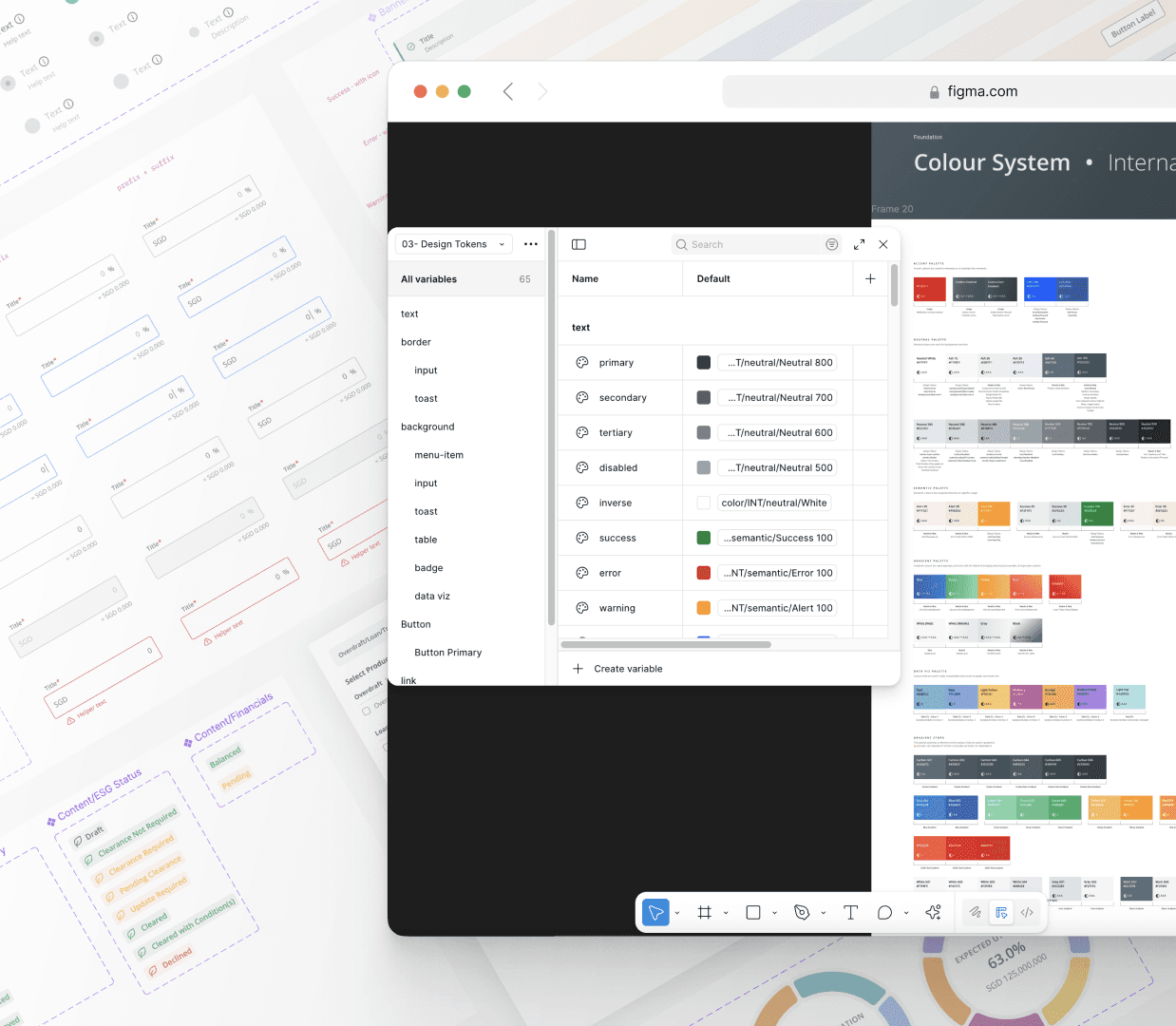

Design Library System

Collaborated with 2 designers to revamp the Internal Design System, aligning components and patterns to the Bank’s Global DS standards. Proposed tokenisation for future scalability, though it was deprioritised due to timeline constraints.

Design Consistency Check

Conducted multi-environment consistency checks across UAT1, UAT2, and Production to ensure platform-wide UI and copy alignment. Drove internal QA documentation and supported developers on identifying and resolving design deviations.

Mobile View for Approvers

Co-designed a mobile-optimised summary view to help Approvers review and approve Credit Applications on the go. Prioritised clarity, key data visibility, and

Retrospective

THE CHALLENGE

Joining mid-project meant inheriting some modules with limited context, outdated components, and minimal documentation. The existing design system, while functional in parts, lacked the robustness and adaptability needed for a data-heavy platform.

Alongside this, I navigated the ambiguity of constantly evolving requirements, shaped by additional business requirements, policy changes, process refinements, and downstream system considerations. This required balancing immediate delivery with maintaining platform-wide consistency and scalability.

Product Owners were ex-Relationship Managers with deep domain expertise but no prior product experience, which often meant requirements and logic were not fully defined upfront. As a result, requirements were frequently revisited or refined during the design process. Each PO had a different working style, requiring designers to adapt while still upholding design standards and ensuring quality through to implementation.

Designing for a high-load enterprise platform also introduced technical challenges: understanding how backend services exchange data with the frontend, how databases are structured, and how different systems integrate was essential to making informed, scalable design decisions.

Key Learnings

Contributing to transformation: Played an active role in modernising the bank’s loan origination system, gathering requirements directly from POs and translating them into scalable, user-centred solutions.

Working with ambiguity: Adapted to constantly changing requirements while considering business decisions, data migration, and downstream impacts.

Designing in flux: Balanced evolving requirements with consistent user experience, business alignment, and technical feasibility.

Scaling in complexity: Created flows and structures that worked across 7 squads, identifying cross-module dependencies and ensuring design consistency with fellow designers.

Challenging assumptions: Learned that design simplicity, if misaligned with user mental models, can hinder usability.

Takeaway

In enterprise platforms, impactful design comes from aligning shifting business needs with consistent, contextually accurate user experiences, ensuring every design decision supports both the organisation’s strategic goals and the user’s operational reality.

More works

Responsive Design | UX | 2023

Aqua Expeditions Website Revamp

Redesigned Aqua Expeditions’ website to streamline discovery, improve booking, and align content architecture with user behaviours and business goals.

Mobile App | UI/UX | Dec 2021 - Mar 2023

AMEX Wallet Experiences

Enhancing the mobile wallet and payment experiences by streamlining card provisioning, introducing secure features, and exploring new features to deepen engagement.

→